This is a very important step for the success of your enterprise. In the marketplace, the companies consider different elements during determining their product’s/services’ price as value for money, quality, uniqueness, differentiation and customer choice.

For many social enterprises their marketplace is in contracting with the public sector to deliver a range of services to benefit their target groups and communities in areas like: support to disadvantaged groups, families, children, disabled people and older people to name but a few.

The present trend in the marketplace is “more for less” money which means you provide more functions, features, services etc. but you get less money than the normal price. Thus, your business has to tackle these challenges. The unit price is generally determined in the contract and the business has to find suitable components or raw materials or suppliers to have its costs in-line with that price if it wants to do the work.

The products/services pricing can be based on three critical points:

What is your products’/service’s value to your customers?

What is the cost of your product/service?

- Your competitors price

Normally, you need to set your product/service price based on your cost structure but you may charge much more (e.g., if you are the first provider in the market) or much less depending on your position based on above critical points.

There are two types of costs in businesses as fixed and variable.

- Fixed (indirect or standing or overheads) costs – these are costs that are always there; like rent, heating, lightning and remain constant, regardless of how much or little you sell (e.g., rent, salaries, business rates).

- Variable (direct or running) costs – these are costs like raw materials or components which increase when your sales increase because they are the costs associated with delivering the product/service. The more you do the more it costs you.

It is necessary to know which costs are fixed and which are variable before you can start to determine the true production costs of a product, or how much it costs to deliver a service. Basically, your fixed and variable costs consist of materials / components, direct labor, overheads, R&D, marketing and distribution and general management items.

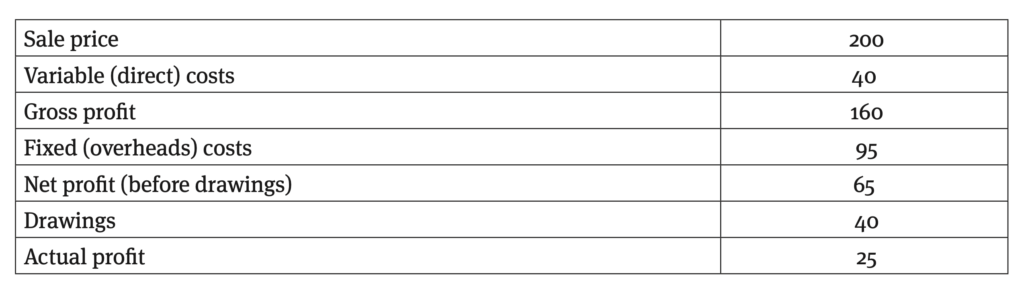

A typical costing might look like this: